China is set to consolidate its position as the dominant country in the automotive industry as a result of developing cutting-edge battery technology for use in electric vehicles (EVs).

The country is already the leader in EV production, with GlobalData’s Global Light Vehicle Hybrid and EV database indicating an EV and hybrid sales volume of 11.42 million for 2023, nearly three and a half times more that of the next nearest country, the US with 3.35 million.

Go deeper with GlobalData

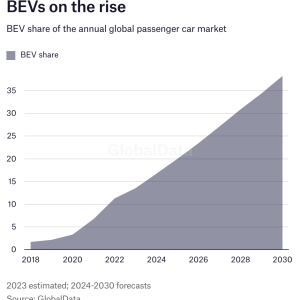

The EV industry remains relatively nascent, however, and sales figures are expected to grow rapidly at a compound rate of 16.1% between 2023 and 2028, reaching 53.9 million, according to GlobalData’s Automotive Predictions 2024 report.

During this period, battery electric vehicle (BEV) production is expected to overtake that of hybrids (HEVs), and China is already well placed to take advantage of this due to its scale, its plentiful supply of the critical minerals required for battery production and the strategic efforts of the country’s government in encouraging collaboration between companies.

China’s EV battery technology

Of the outlook for China, Tom Bloor, managing director at EV charging company Evec, tells Just Auto: “China is leading the way in EV sales. Currently. it has 60% of global sales. Its new EV sales increased by 82% in 2022, and I predict this will only increase over the next year.

“What is going to steer the global growth of EV is battery technology. Manufacturers who can produce batteries offering more mileage and performance take a huge portion of the market. Battery range is one of the most important considerations for somebody choosing an electric car. If BYD could offer a 600-mile range but Tesla only 400 miles, most people would purchase a BYD – and would encourage the petrol/diesel drivers to move over if the range is longer than a tank of fuel.”

US Tariffs are shifting - will you react or anticipate?

Don’t let policy changes catch you off guard. Stay proactive with real-time data and expert analysis.

By GlobalDataIndeed, BYD is one of a host of major Chinese EV manufacturers that have joined a government-led alliance to speed up the development of solid-state batteries, which are expected to revolutionize the EV industry.

Solid-state batteries (SSB) work in much the same way as conventional lithium-ion batteries but use a solid rather than liquid electrolyte – most commonly in those being produced for EVs sodium-ion. Though they remain some way off, with the first SSB-powered vehicles only expected to hit the roads in 2025, they are widely heralded as being the next leap forward in EV battery tech through being lighter, able to hold more energy, quicker to charge, safer and long-lasting.

The China All-Solid-State Battery Collaborative Innovation Platform (CASIP) alliance is “aimed at leading the world in solid-state battery technology” and reportedly counts six of the top 10 automotive battery makers globally among its members.

Of the CASIP initiative, Chen Qingtai, head of the China EV100 for exploring industrial policy about EVs, is quoted by Nikkei as saying that “China has been leading the world in new-energy vehicles because of its advanced battery technology,” and that it should prioritise new solid-state battery technology to build on that position.

Chen’s assertion carries weight – GlobalData’s Automotive Predictions report states that “In 2023, China accounted for 73% of global battery cell production destined for light vehicle BEV fitment.” While that figure is expected to fall as competition grows elsewhere, the country is expected to remain the top global BEV battery cell supplier through the decade in terms of output.

Solid-state EV battery technology

Elaborating on this, GlobalData powertrain expert analyst Oliver Petschenyk tells Just Auto: “China is dominant in production of the budget-friendly cobalt-free battery solutions, lithium iron phosphate (LFP) for example, which as it stands is a proven low-cost chemistry that adheres to a lot of automotive like to haves such as low cost, high life cycle capability and good safety, is predominantly produced in China.

“We see some LFP-powered models at very similar price points to the internal combustion engine (ICE) equivalent segment, especially when compound with the fact ICE vehicles are becoming more expensive, partly due to emissions regs, but I believe sodium-ion will be key to BEVs becoming cheaper than ICE. It has very low energy density but, when coupled with LFP cell-packing density, does appear to make a viable solution.

“At present it’s only targeted at superminis, but I believe that as soon as technology advances in sodium-ion – still very much in its infancy – it could become the dominant technology for non-long range/performance EVs (aka budget EVs). As far as I’m aware only two plants are planned outside of China, so again China is ‘ahead of the game’ on this technology too.”

Notably, Petschenyk is not convinced SSBs are as yet ready for mass manufacture without losing some associated benefits, noting that Toyota has been pushing back its much-heralded SSB plans for years.

“There are too many tolerancing and uniformity concerns for mass production of ceramic-based SSBs, and polymer-based cells appear to have lower power capability or temperature performance issues. I don’t doubt an OEM will come to the table with a solid-state cell soon, but I don’t believe they will be as groundbreaking as everyone is hoping – yet.

“I am, however, gaining confidence in semi-solid cells becoming more popular. They offer increasing energy density and performance with extremely high safety and minimal tolerancing issues, making mass production more viable.

“And again all known and planned production is coming from China. We expect China to maintain the majority share of battery production and this will leverage BEV production volume.”